Many M&A deals are premised on the value of synergies. In some cases, synergy targets can be as high as 30% to 70% to justify the deal. Yet synergies are often overvalued. Clearly, when that happens deals don’t live up to their promise and destroy significant shareholder value instead. As part of the strategic due diligence process, we look at four best practices that get to the heart of common synergy valuation problems, and ensure that synergies are valued correctly.

SYNERGY VALUATION IN CONTEXT

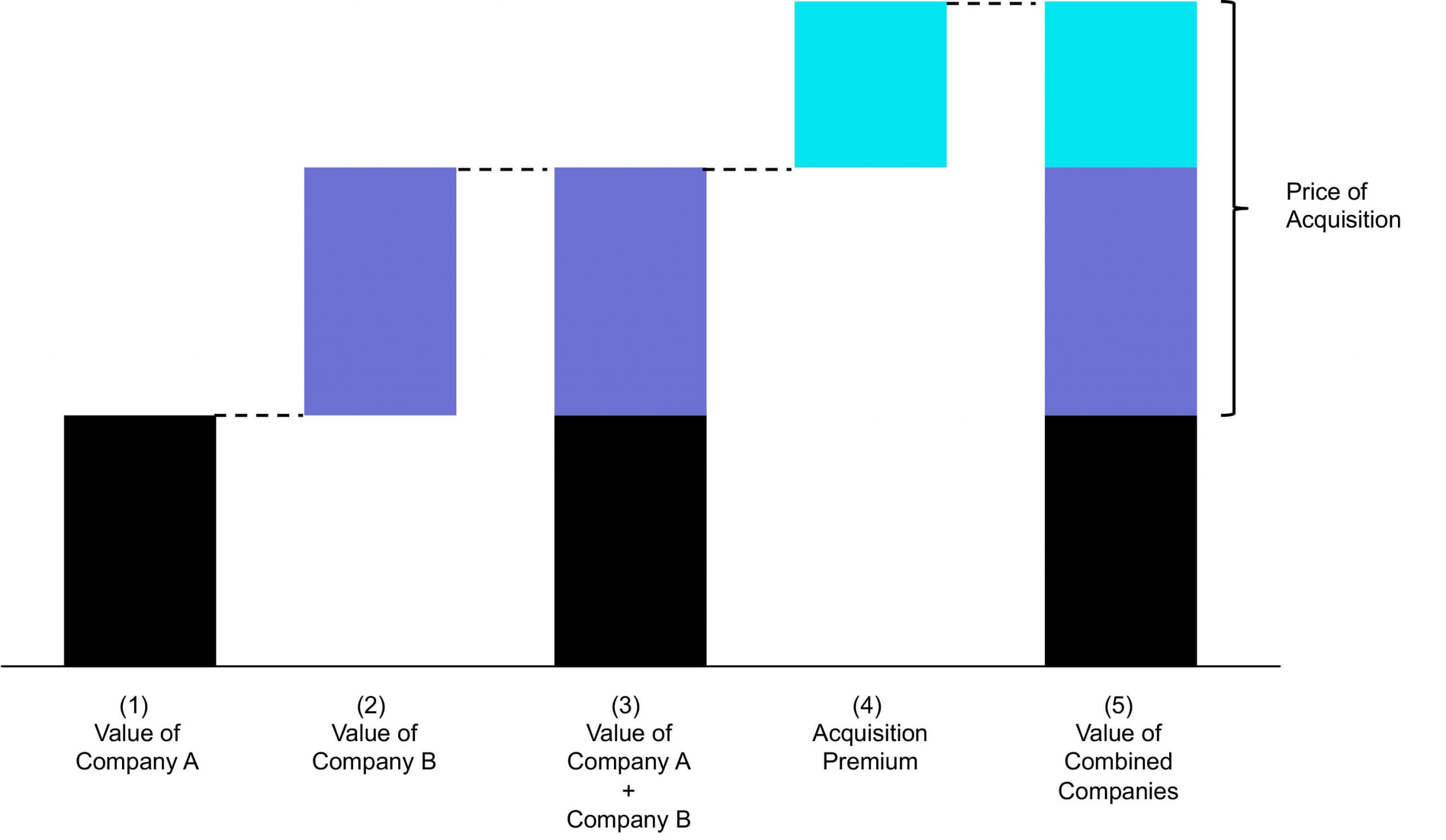

The value of two merged companies is the sum of the value of the acquiring company plus the value of the target company plus the acquisition premium, which includes the synergies created. The price of the acquisition is the sum of the value of the target company plus the acquisition premium (Figure 1).

Fig. 1 The Components of an M&A Deal

For the purpose of this discussion, we classify synergies in two broad groups: operating synergies and financial synergies. Operating synergies impact cost, revenue growth, pricing power, net working capital, and fixed assets, and contribute to higher cash flows. Operating synergies are valued within the framework of the combined discounted cash flows of the merged entities.

Financial synergies include improved capital structure, diversified risk, tax reduction, and use of cash. They are valued within the framework of the capital structure of the merged entities (including debt, equity, lower tax, lower risk premium) or the anticipated returns for the cash put to use.

BEST PRACTICES

We look at four best practices in valuing synergies to avoid leaving millions of dollars on the table. The approach is to value synergies as inputs to the Discounted Cash Flow model and use the following rules.

Use the right discount rate: From time to time, analysts use the discount rate of either the target company or the acquiring company in valuing synergies. Either one is incorrect. Synergies should be valued by using the discount rate of the combined entities. The combined discount rate reflects the true nature of the project, which requires the merged entities to produce the synergies.

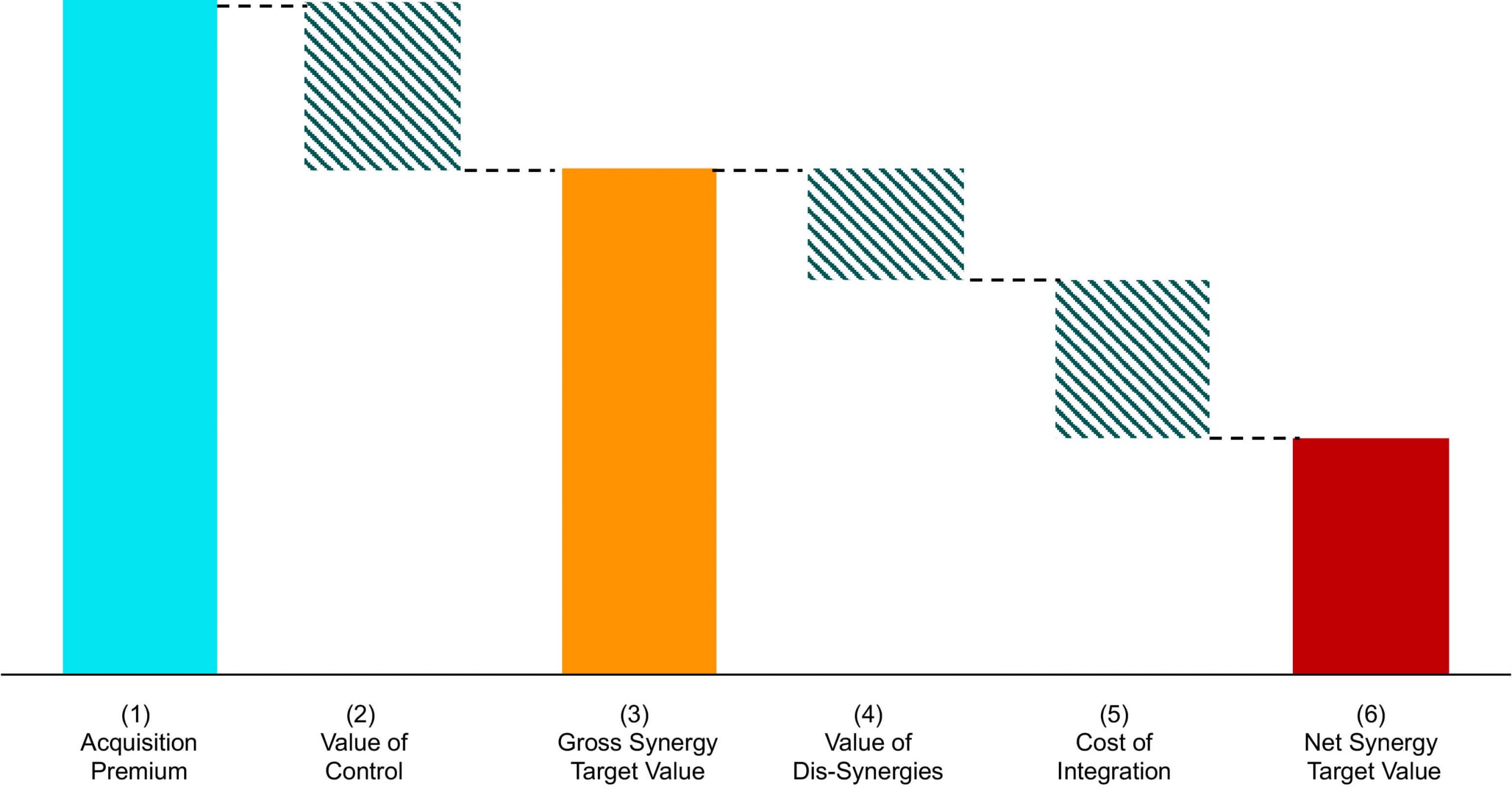

Isolate the value of control from the value of synergies: The control premium reflects the incremental value that the acquiring company can create by managing the target company better or more efficiently. The value of control reflects better management. The value of synergies reflects the combinatorial effects of two merged entities. Mixing the value of control and the value of synergies is inaccurate. They are separate concepts with separate effects, which must be treated separately: discount the control premium at the acquirer’s discount rate; and discount the value of the synergies at the combined discount rate of the two firms. Anything different can inject errors of double counting.

Subtract the value of dis-synergies: There are inherent ‘dis-synergies’ to any M&A deal. These items are losses expected to materialize as a result of the merger. Typical dis-synergies include the following: loss of customers; defection of quality employees to the competition; re-adjustment of employee benefits if the acquirer has better ones than the seller; cost of re-aligning reporting structures; re-branding; disposition of some assets based on antitrust considerations, and more. The value of dis-synergies must be subtracted from the value of synergies.

Subtract the cost of integration: Synergies don’t happen by chance. It takes integrating the two companies to deliver the value of synergies. There are many types of integration depending on the scope of the M&A deal. In a functional integration, companies merge key operating functions (e.g. human resources, legal, accounting) leaving the rest of the business intact. In a full operational integration, merging takes a change of control, senior management changes, primary activities, support functions, and occasionally restructuring. Whichever type of integration is required, merging comes at a cost and the timing of the benefits is not immediate. The cost of integration must be subtracted from the gross synergy target value, and expectations of the realization of benefits must be timed realistically (Figure 2).

Fig. 2 Estimating Net Synergies

These best practices will lead to a more realistic valuation of the deal’s synergies and, ultimately, the acquisition price.