A leading supplier of refrigerated logistics services wanted to enter the French market, viewed as a lucrative opportunity. The company was specialized in temperature-controlled food distribution, including chilled and frozen temperature ranges. Management needed to know if there was room to enter, where to enter, how to establish an entry point, build competitive advantage and defend against competitive retaliation.

The company entered the French market successfully based on the following recommendations:

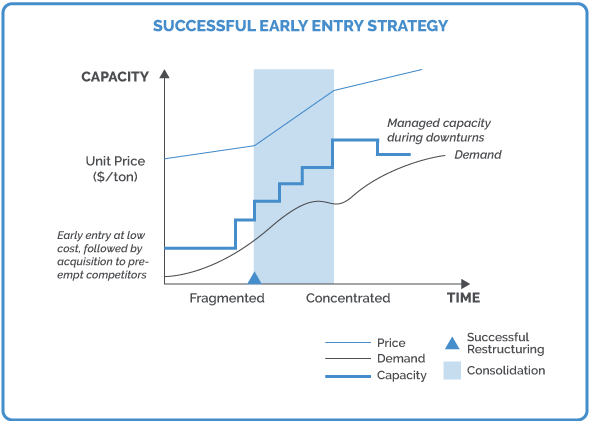

- Enter the chilled sector: it was fragmented, growing and demand exceeded supply; conversely the frozen sector was consolidated and flat

- Position the company as a logistics service supplier to food retailers, as opposed to serving food suppliers who were not quality sensitive

- Because retailers were not satisfied with current offerings and were willing to switch suppliers, offer a competitive value proposition based on quality of service, including: full service, best-in-class time-definite service, and national coverage

- Full service needs to include

- transport (long haul, express delivery),

- warehousing (warehouse management, platform management, accessory services)

- imports and exports

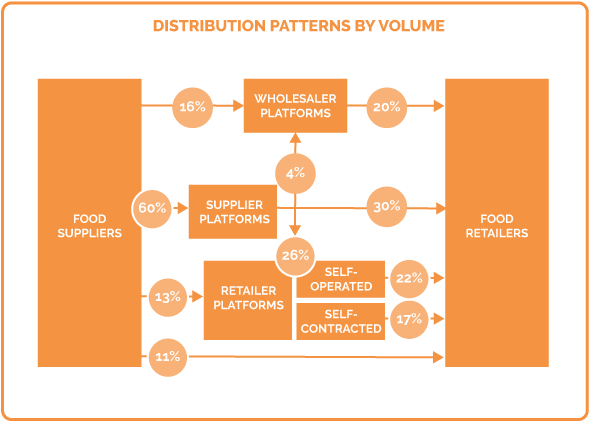

- Target the most attractive distribution channel: retailers specialized in hypermarkets and supermarkets, particularly those with low chain concentration and higher need for logistics

- Focus on moving an effective product mix of chilled foods (co-transportable, back-to-back transportable), to include primarily meats and dairy

- Secure access to national network of logistics platforms in order to be able to compete effectively on a national scale

- Acquire two regional logistics companies to form a national entity in order to:

- secure access to a national network of logistics platforms

- exploit existing relationships with retailers

- minimize retaliation against a new foreign entrant

- Continue to build scale through acquisitions

Over the next five years, the company became the second largest service provider in the country.

We conducted a strategic assessment of the market opportunity and identified target acquisitions.

INDUSTRY ANALYSIS

- Analyzed industry structure, key markets, axes of competition and strategic groups

- Segmented market for logistics services by logistic activity (dedicated warehousing, cold storage, contract freight management, long-haul delivery, express delivery), by food group, and by customer type (supplier, retailer)

CUSTOMER ANALYSIS

- Conducted field interviews to determine key purchase criteria, level of satisfaction, competitive quality ratings

MARKET ANALYSIS

- Sized market and growth

- Analyzed market price structure and price sensitivity

- Analyzed the food retail market, segments, key players, including size, growth and trends

- Identified requirements and assets to build competitive position, including truck fleet, warehouses and logistics platforms

IDENTIFICATION OF KEY SUCCESS FACTORS

- For each asset, determined key success factors, including:

– products co-transportable and back-to-back transportable (vegetables, dairy) for maximum utilization of truck fleet;

– ownership of warehouses and logistics platforms in key geographical locations

SCENARIO ANALYSIS

- Explored various entry options

Recommended acquisition of two regional companies to establish national network

Prepared screening criteria and a short list of candidate target companies