Companies are squeezed for profits all the time. Pressure comes from multiple fronts: customers have more information making pricing more transparent; product proliferation is increasing cost to serve; globalization is creating a new class of competitors; digitization is changing the business model softening barriers between sectors; competitors’ actions are more diverse and more complex to predict than just five years ago, requiring quicker responses and increased deployment of resources; new technology start-ups are reducing product life cycles; the firm’s organizational structure is growing larger, harder to manage, adding layers of management and more indirect cost; suppliers are getting leaner and more powerful, exerting higher costs of raw materials. The net effect to the firm is downward pressure on prices, ever-increasing costs, and larger deployment of resources.

TAKE A STRATEGIC VIEW

The reality is that not every dollar of cost is equal. Some costs drive customer value creation and profits directly; others do not. The goal is to know which costs, activities, and efforts yield the optimal return to the firm and its stakeholders.

Traditional cost reduction offers improvements regarding efficiency and productivity and their impact on the bottom line. While helpful, traditional costing takes a short-term view of costs. As such, it doesn’t get to fundamental issues about cost that companies need to be able to address to run their business. Some of these include the following: What is the net profitability of each product line? What are the true costs of serving customers? What drives the costs that exist? Is the company value chain configured for maximum effectiveness? These questions are unanswerable by standard costing.

Strategic costing identifies costs that the company doesn’t need to carry, enabling management to eliminate large chunks of unnecessary cost altogether. These are items that traditional costing cannot see. Some of these include the following: eliminating unprofitable products, rationalizing unprofitable customers, reconfiguring the company value chain of activities, cutting back low-return capital investments, simplifying the organizational structure of the firm, reducing spend, pricing strategically, and much more. Whereas traditional costing operates on functions as the objects of improvement, strategic costing operates on three objects: the company’s products, its value chain, and its resources.

EXTRACT VALUE

The business core must be lean and sell profitable products to profitable customers. To get there, products must be rationalized; the company value chain of activities must be made effective; and resources need to be rationed effectively.

- Rationalize Products: As the product technology stabilizes, matures, and becomes adopted in the industry, two realities set in that drive the cost of complexity: product proliferation and shorter product life cycles. Product proliferation develops as companies offer larger product variety to penetrate smaller market segments. Shorter product life cycles appear as companies renew products to keep up with faster technological development. In either case, a trade-off exists between revenue and the company’s cost position. Some companies may find themselves offering too many products or updating products too often, actually hurting profitability – in which case products must be rationalized. Deciding how much product variety to offer and how often to renew products are strategic decisions that get to the core of company profitability.

- Rethink the Value Chain: The value in identifying and analyzing activities that consume valuable resources lies in the fact that not all activities add value to a company’s products and services. This realization offers managers the opportunity to optimize value-added activities and processes, and eliminate non-value-added activities and processes in all functional areas of the value chain, removing duplication, reducing process cycle time, and outsourcing non-core processes. The objective is the achievement of competitive advantage and value offered to customers based on a deliberate strategic choice.

- Ration Resources: Resources or “means of production” include plants, property, equipment, labor, working capital, material, energy, information, intangible assets, and more. Resources cost money; therefore, management must use them effectively and efficiently in meeting customer needs. The cost structure of the company is directly impacted by the use of resources, which explains why they are objects of strategic costing.

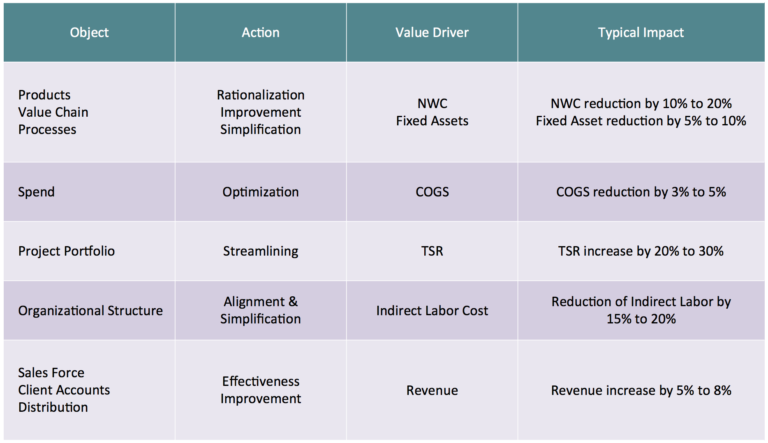

With these measures in place, subsequent improvements follow. Spend can be paired down to fit the reduced number of product lines, lowering COGS considerably. The company’s project portfolio can be streamlined to fit the business strategy and NPV standards, increasing total shareholder returns. The organization can be aligned with the business strategy and simplified, trimming indirect labor costs. Pricing, the sales force, and customer accounts can be aligned to the business for maximum effectiveness, lifting profitability and increasing revenue. In sum, strategic cost leverage confers tremendous opportunity to create value.

EXHIBIT 1. STRATEGIC COST LEVERAGE

Source: Great Prairie Group