Leaders need to take an objective look at their corporate portfolio at the onset of an economic slowdown. The dynamics of slowing sales and falling profits put pressure on them to take proactive steps early on to strengthen the strategic position and the balance sheet of the company. However, many obstacles stand in the way of managing the portfolio proactively.

THE SITUATION

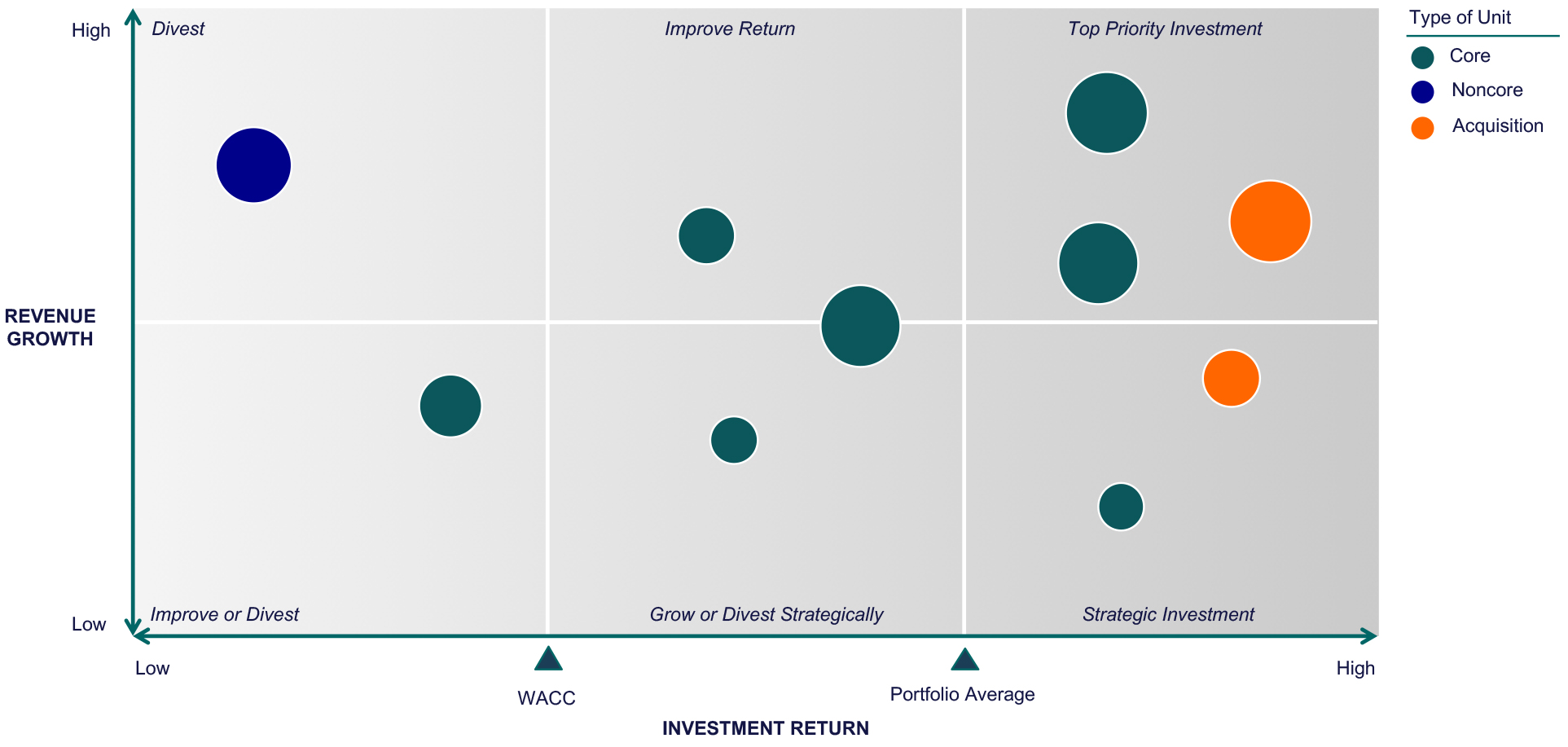

A preliminary disaggregation of the corporate portfolio into the individual units provides a useful top-down view of overall performance, combining return and revenue growth by each unit. Exhibit 1 shows an example.

Exhibit 1. Portfolio Performance by Business Unit

Returns above the average cost of capital (WACC) make for the creation of value, while returns below the WACC make for the destruction of value. Together, measures of investment return and revenue growth provide a frame of reference for the unit’s performance and the overall portfolio.

THE IMPACT OF AN ECONOMIC SLOWDOWN

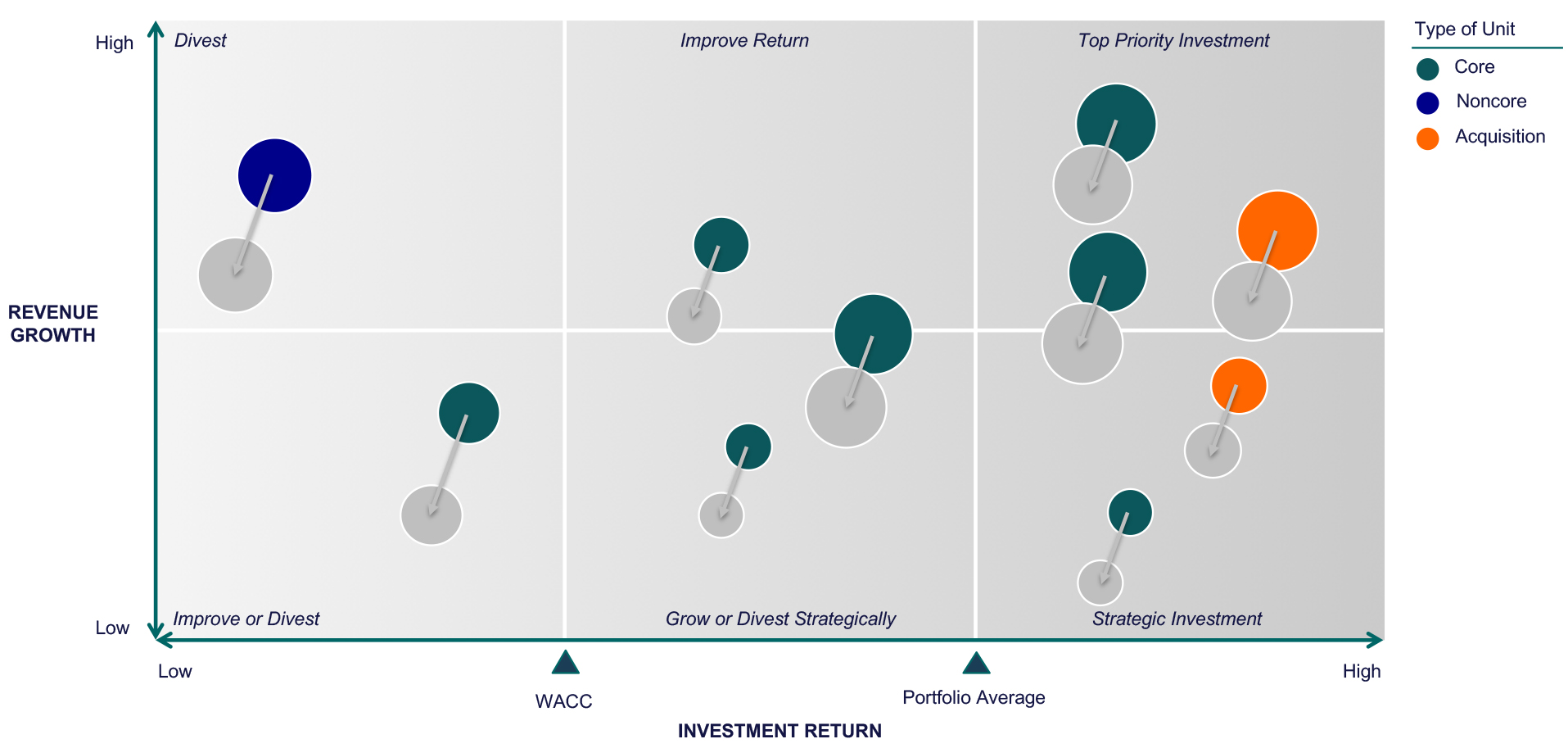

The performance of the corporate portfolio deteriorates during an economic slowdown as revenues stall, profits fall, returns decrease, and valuations drop (Exhibit 2). Each unit is affected differently, but the collective performance of the portfolio declines, which is deeply concerning.

Exhibit 2. Impact of an Economic Slowdown on Portfolio Performance by Business Unit

On the one hand, non-performing units become far more challenging to fix. On the other hand, given a slowing economy, divestitures become more drawn out as buyers usually wait until the market bottoms out before buying. In both cases, waiting to take action lowers the ability of the firm to take meaningful action. If left unattended, this condition eventually drains financial resources from the company and limits the number of options available to improve the situation. This limitation can be tackled upfront and clear-headedly.

THE CHALLENGE

It is essential for management to confront the slowdown early on before it gets into full swing. By managing the portfolio proactively, leaders can drive the company to a position of strength, generate value, and build the capital reserves that the firm will need later on. The program takes divesting specific units, fixing others, focusing resources on growth businesses, and building capital reserves for acquisitions for later, during the economic recovery. Many internal obstacles stand in the way, however.

Firstly, CEOs are rewarded for growing companies, not shrinking them. Divesting units ahead of a slowdown requires a disciplined approach and the promise of re-investment at a later time. This type of program doesn’t exist within the company, unlike programs that promote growth plans. So, boards are not always convinced. Similarly, shareholders don’t want to see a contraction of sales or assets. As a result, the CEO may find it risky to stake his leadership on this course of action and prefer to play it safe, following along with most companies in the market.

CONCLUDING REMARKS

Three steps can help executive management get beyond this type of impasse:

- Present an accurate picture of the portfolio context, including markets, growing and maturing businesses, and investment options

- Formulate decision making based on transparent analytical rigor and a robust portfolio strategy

- Apply ruthless capital discipline that shows financial restraint based on reasonable projections

These steps go a long way toward helping corporate leaders explain the rationale for setting the portfolio direction. Winning companies embrace this type of disciplined approach, including TMSC, Ford, AB InBev, Home Depot, and Verizon, to name a few. Others stall and grow weaker.

What is your next move?

How will you decide your timing to take action?