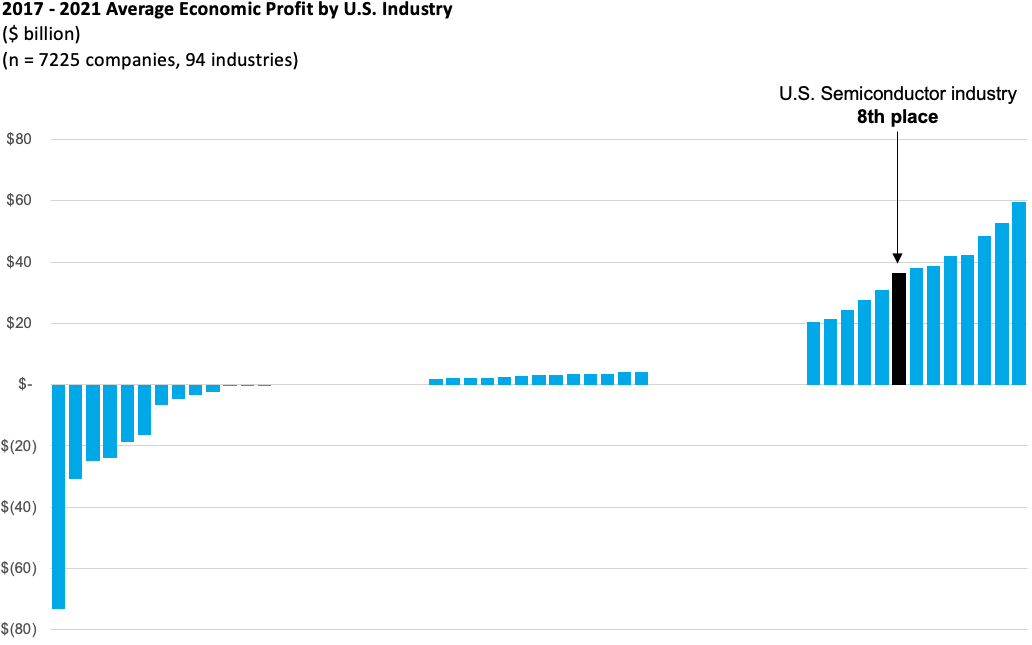

The U.S. semiconductor industry is a global semiconductor supply chain leader. The industry is one of the largest producers of economic profit in the U.S., with an outstanding performance in 2021 and ready for considerable growth in the next ten years.

INDUSTRY PERFORMANCE

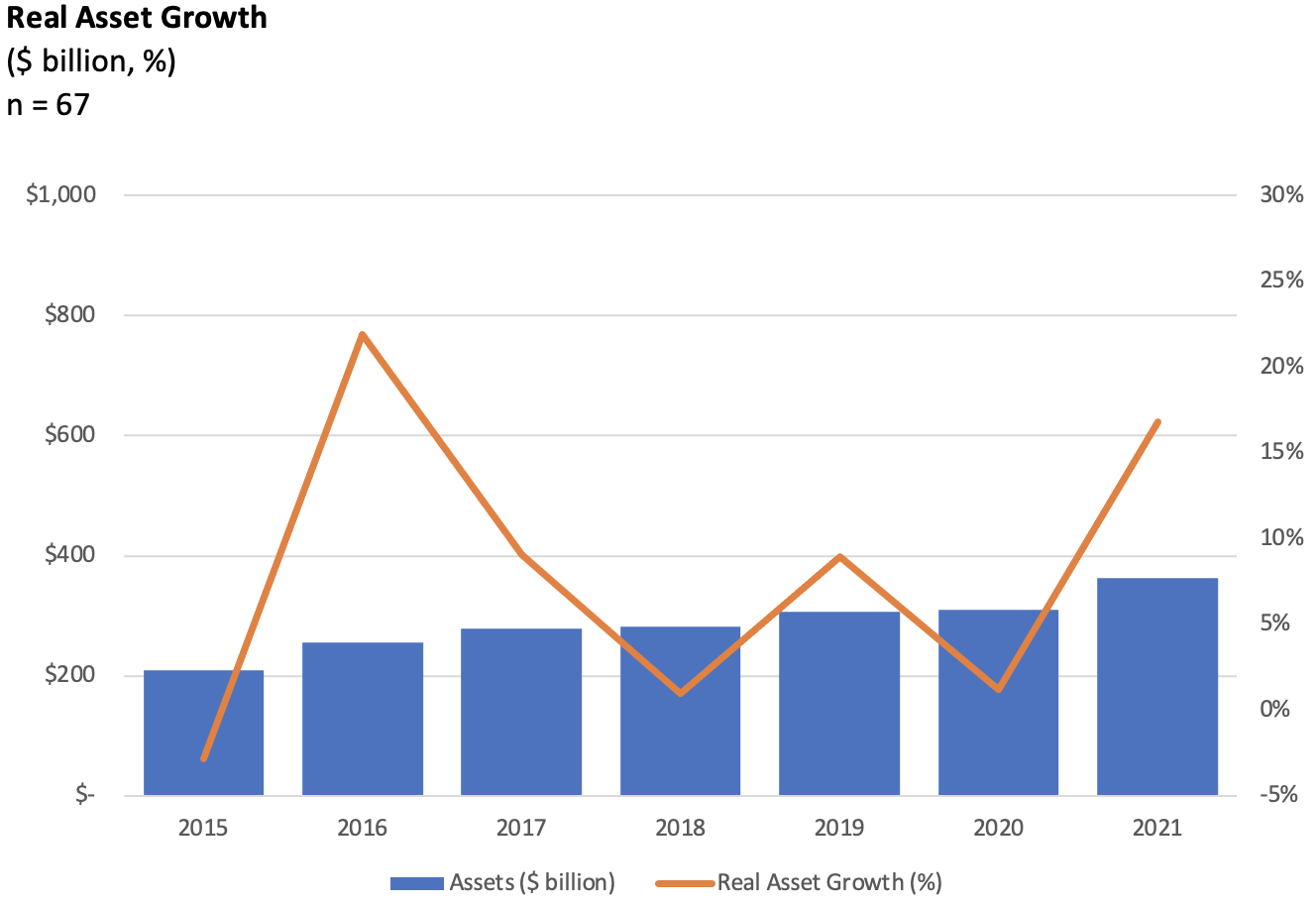

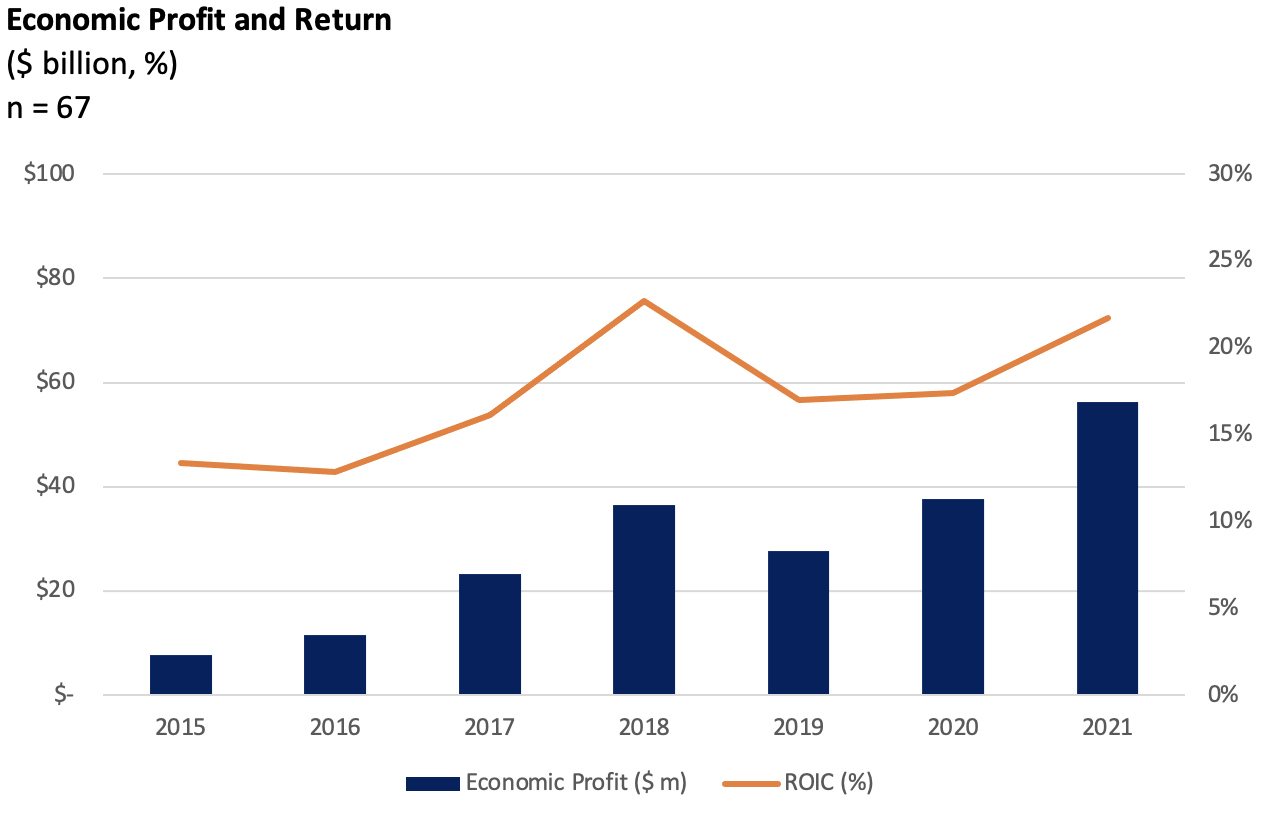

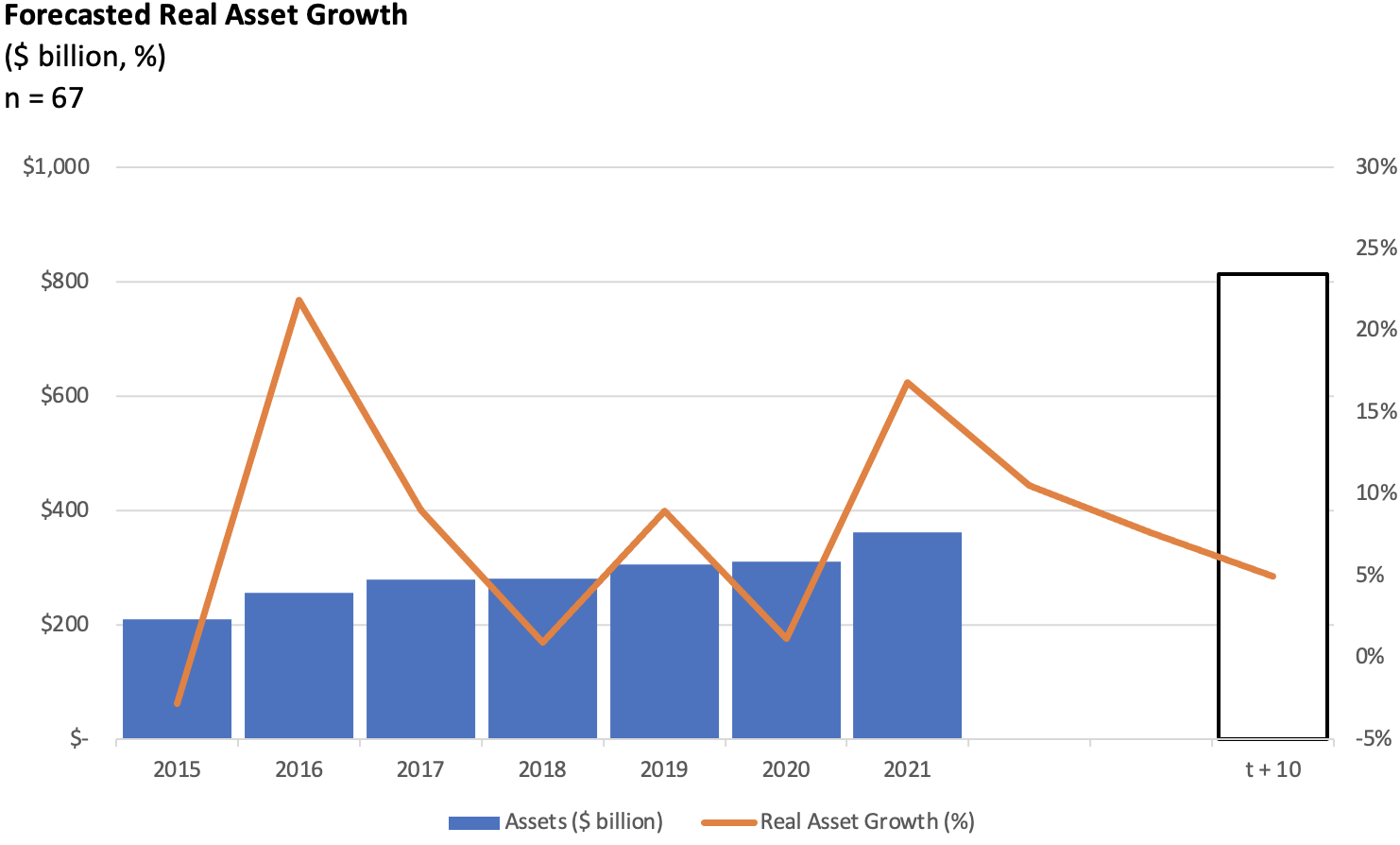

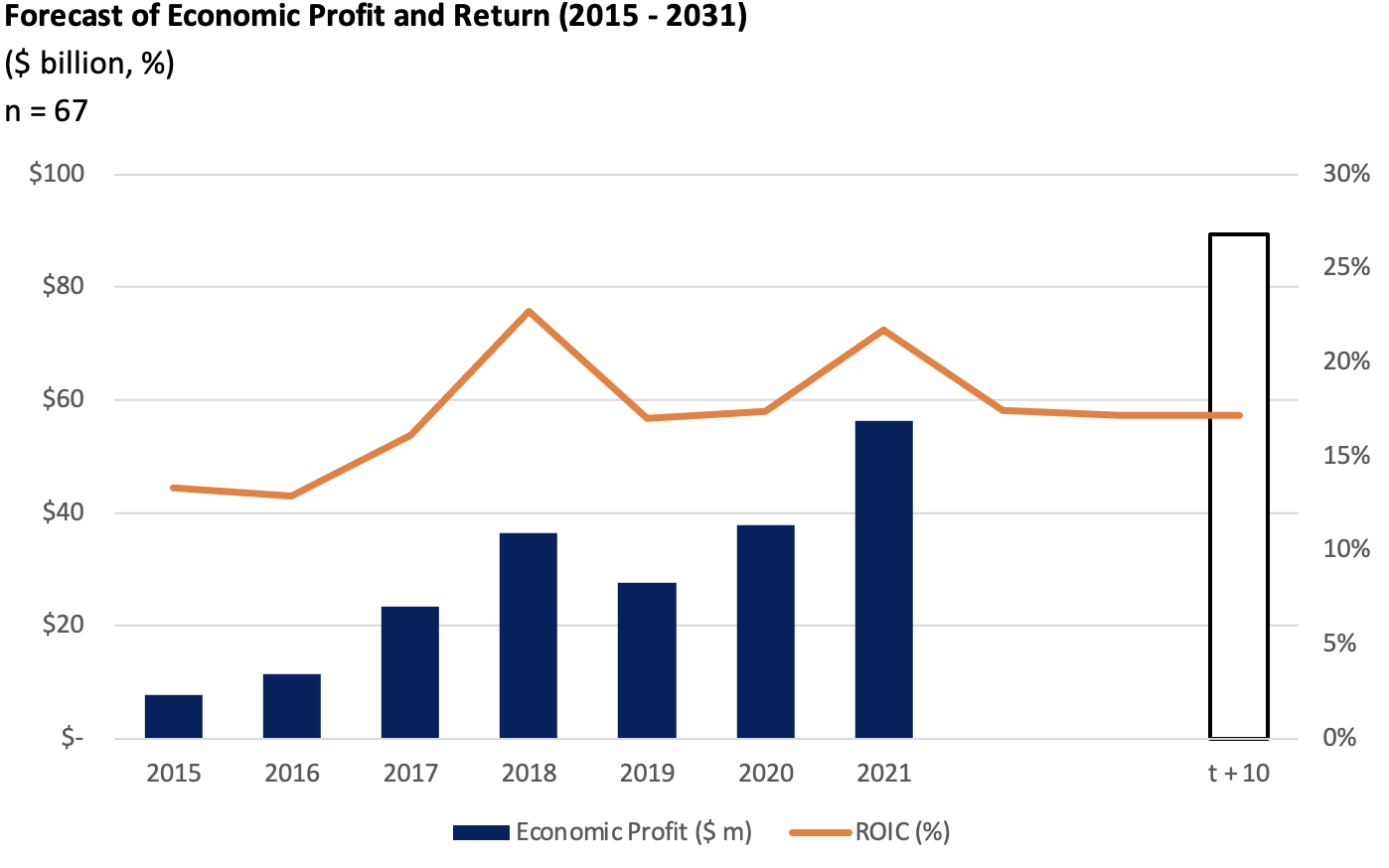

The U.S. semiconductor industry has been improving its performance steadily since 2019, with a sudden take-off in 2021. Assets grew by 14.7% in 2021 to $360 billion, generating the highest level of growth in five years. Economic profit increased from $38 billion in 2020 to $56 billion in 2021, and ROIC rose from 17.4% to 21.7% in the same period.

Exhibit 1. U.S. SEMICONDUCTORS INDUSTRY VALUE CREATION PERFORMANCE CHART

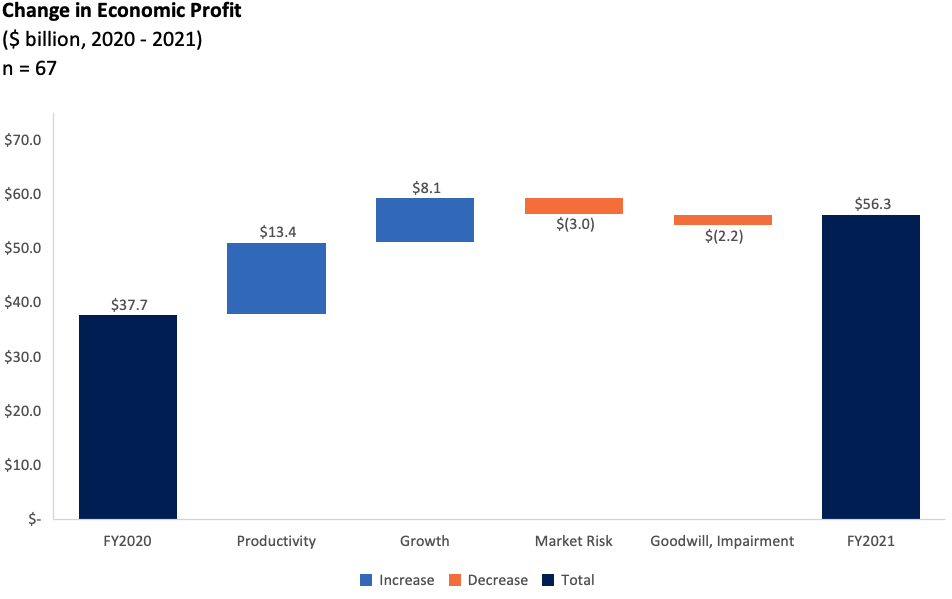

In 2021, the industry gained $18.5 billion in economic profit, representing an improvement of roughly 50% from 2020. Productivity and growth increased economic profit by $13 billion and $8 billion. An increase in the industry’s cost of capital, i.e., market risk, accounted for a decrease of $3 billion. Finally, acquisitions, as reflected in goodwill and impairment, drove a reduction in economic profit of $2 billion. Overall, the net situation is a healthy position for the industry, poised for growth in 2022.

INDUSTRY OUTLOOK

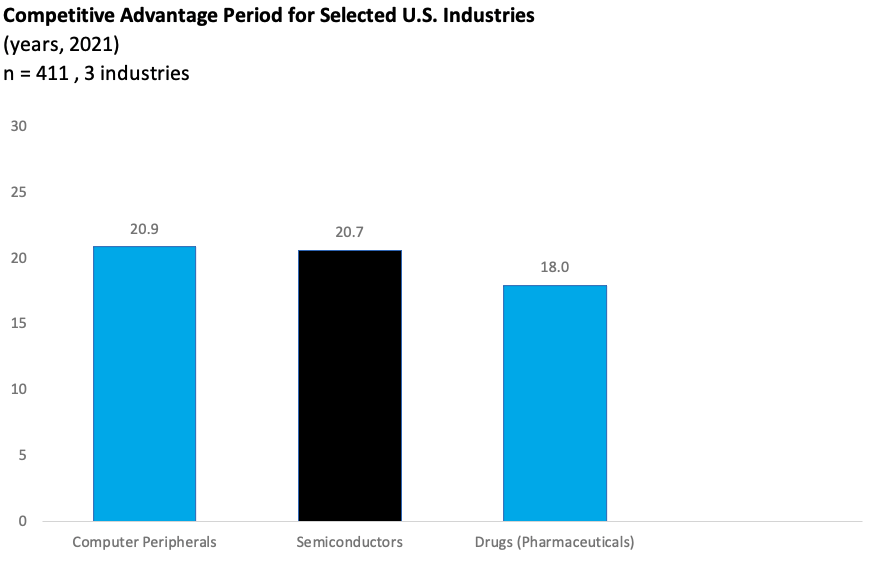

The outlook for the industry is positive. The industry’s competitive advantage period (CAP) is 21 years, as implied by the market. The CAP represents the sustainability of the competitive advantage intrinsic to the industry. It measures the number of years the industry can maintain a competitive edge against new entrants and the spread between return on capital and cost of capital.

The industry CAP of 21 years is due partly to high competitive barriers, including the high level of complex technologies content and the need for operational scale on the one hand, and partly to exposure to the risk of disruption of the global supply chain on the other. More on this later.

Exhibit 2. U.S. SEMICONDUCTORS INDUSTRY VALUE CREATION FORECAST CHART

The market-implied real growth is projected to achieve a CAGR of 8.4% in the next ten years, increasing assets to $810 billion by 2031. The market-implied economic profit for the industry is expected to reach $89 billion by 2031 – an increase of nearly 60% from $56 billion in 2021.

Demand for semiconductors is highly global, with the U.S. and China comprising the most significant markets. Growth will be driven primarily by four sectors: automotive, information and communications technology infrastructure, mobile phones, and industrial electronics.

The supply chain of semiconductors is also global. The implication means that companies are interdependent across geographies, including the U.S., East Asia (i.e., Taiwan, South Korea, and Japan), the E.U., and China. Today, 75% of the installed manufacturing capacity is in East Asia and China. Such a high capacity concentration in geographies with geopolitical tensions raises the risk of disruption.

WHAT DOES THIS MEAN FOR MANAGERS?

Given the positive outlook of the U.S. semiconductor industry, the mandate for managers will be to decide which areas to pursue while balancing the pursuit of leadership in their core market and resiliency against exposure to global geopolitical tensions. Four business models have emerged to deal with technological complexity and the need for scale:

- Integrated Device Manufacturers (IDMs) are vertically integrated across the value chain, including design, manufacturing, assembly, packing, and testing

- Fabless firms specialize in design with outsourced fabrication, assembly, packaging, and testing,

- Foundries address fabrication needs for fabless firms and IDMs with insufficient manufacturing capacity, and

- Outsourced Assembly and Testing (OSAT) companies provide assembly, testing, and packaging under contract for IDMs and fabless companies.

Whichever the business model, by integrating strategic and financial assessments, managers can develop insights into where the company has a strong likelihood to succeed and the most realistic path to add value and sustain competitive advantage. Findings will reveal target opportunities and areas for R&D investments, added manufacturing capacity, and potential M&As and strategic alliances to augment growth capabilities.